Economics and Business Analysis: Foundational Principles Study Guide

This study material has been compiled and organized from a lecture audio transcript and a copy-pasted text containing key definitions and questions.

📚 Introduction to Economic Principles

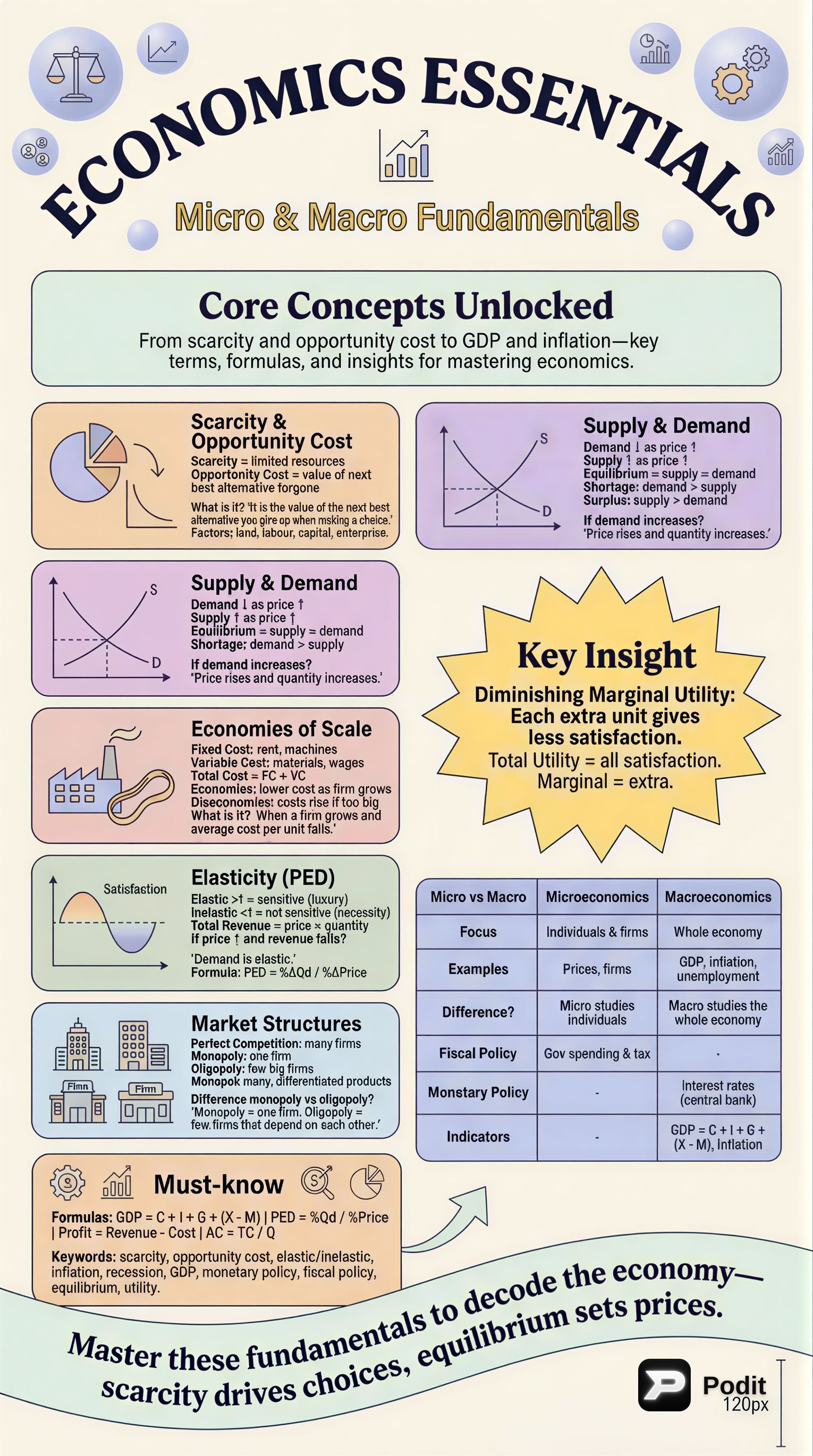

Economics is a fundamental field that examines how societies allocate scarce resources to satisfy unlimited wants and needs. It is broadly divided into two main branches: Microeconomics and Macroeconomics. Understanding these principles is crucial for comprehending individual and firm decisions, market functions, and the performance of entire national economies. This guide covers core concepts from both microeconomic and macroeconomic theory, alongside essential frameworks for business analysis.

🔬 Microeconomic Concepts: Individuals, Firms, and Markets

Microeconomics focuses on the behavior of individual economic agents, such as households and firms, and how they interact in specific markets.

1. Scarcity, Choice, and Opportunity Cost

The foundation of economics lies in scarcity 🌍, meaning resources are limited while human wants are unlimited. This necessitates making choices ✅.

- Scarcity: The fundamental economic problem of having seemingly unlimited human wants and needs in a world of limited resources.

- Choice: The act of selecting among alternatives due to scarcity.

- Opportunity Cost: The value of the next best alternative that must be given up when a choice is made. It's what you forgo to get something else.

- Example: If you choose to study for an exam, the opportunity cost might be the income you could have earned working during that time.

- Allocation: How limited resources (land, labor, capital, enterprise) are distributed and utilized among competing uses.

- Factors of Production:

- Land: Natural resources.

- Labor: Human effort.

- Capital: Man-made resources used in production (e.g., machinery).

- Enterprise: The ability to organize and manage the other factors of production.

- Factors of Production:

2. Costs and Economies of Scale

Firms face various costs in production:

- Fixed Cost (FC): Costs that do not change with the level of output (e.g., rent, machinery depreciation).

- Variable Cost (VC): Costs that change with the level of output (e.g., raw materials, wages for production workers).

- Total Cost (TC): The sum of fixed and variable costs (TC = FC + VC).

- Economies of Scale: Occur when a firm's average cost per unit falls as its output (size) increases. This is often due to specialization, bulk purchasing, or more efficient use of machinery.

- Diseconomies of Scale: Occur when a firm becomes too large, leading to increased average costs per unit. This can be due to coordination problems, bureaucracy, or communication breakdowns.

3. Supply and Demand

These are the fundamental forces that determine market prices and quantities.

- Demand: The quantity of a good or service that consumers are willing and able to purchase at various prices during a specific period.

- Law of Demand: As price increases, quantity demanded decreases (and vice versa).

- Supply: The quantity of a good or service that producers are willing and able to offer for sale at various prices during a specific period.

- Law of Supply: As price increases, quantity supplied increases (and vice versa).

- Equilibrium: The point where the quantity demanded equals the quantity supplied. At this point, there is no tendency for price or quantity to change.

- Shortage: Occurs when quantity demanded exceeds quantity supplied (demand > supply), leading to upward pressure on prices.

- Surplus: Occurs when quantity supplied exceeds quantity demanded (supply > demand), leading to downward pressure on prices.

- 💡 Insight: If demand increases, both the equilibrium price and quantity will generally rise.

4. Elasticity (Price Elasticity of Demand - PED)

Elasticity measures the responsiveness of quantity demanded or supplied to a change in price or other factors.

- Price Elasticity of Demand (PED): Measures how much the quantity demanded of a good responds to a change in its price.

- Elastic Demand (PED > 1): Quantity demanded is highly sensitive to price changes. Often associated with luxury goods or goods with many substitutes.

- Inelastic Demand (PED < 1): Quantity demanded is not very sensitive to price changes. Often associated with necessities or goods with few substitutes.

- Total Revenue (TR): The total income a firm receives from selling its goods (TR = Price × Quantity).

- Example: If price increases and total revenue falls, demand is elastic. Consumers are cutting back significantly on purchases due to the price hike.

5. Utility

Utility refers to the satisfaction or benefit derived from consuming a good or service.

- Total Utility: The overall satisfaction gained from consuming a certain amount of a good.

- Marginal Utility: The additional satisfaction gained from consuming one more unit of a good.

- Diminishing Marginal Utility: The principle that as a consumer consumes more units of a good, the additional satisfaction (marginal utility) gained from each successive unit tends to decrease.

- Example: The first slice of pizza brings immense satisfaction, but the tenth slice might bring very little, or even negative, satisfaction.

6. Market Structures

Market structures describe the competitive environment in which firms operate.

- Perfect Competition: Many small firms, identical products, free entry and exit, price takers.

- Monopolistic Competition: Many firms, differentiated products, relatively easy entry and exit.

- Oligopoly: A few large firms dominate the market, interdependent decision-making, significant barriers to entry.

- Key Difference: A monopoly has only one firm, while an oligopoly has a few large, interdependent firms.

- Monopoly: A single firm dominates the entire market, unique product, significant barriers to entry, price maker.

- Barriers to Entry: Obstacles that make it difficult for new firms to enter a market (e.g., high start-up costs, patents, government regulations).

📈 Macroeconomic Concepts: National Performance and Policy

Macroeconomics examines the economy as a whole, focusing on aggregate phenomena and national economic performance.

1. Micro vs. Macro: The Big Picture

- Microeconomics: Studies individual economic units (households, firms) and specific markets (e.g., the price of cars, a firm's production decisions).

- Macroeconomics: Studies the economy as a whole, focusing on aggregate variables like national output (GDP), inflation, and unemployment.

2. Fiscal and Monetary Policy

Governments and central banks use policies to influence the economy.

- Fiscal Policy: Government's use of spending and taxation to influence the economy.

- Expansionary Fiscal Policy: Increased government spending or reduced taxes to stimulate economic growth.

- Monetary Policy: Central bank's control over interest rates and the money supply to influence economic activity.

- Higher Interest Rates: Reduce borrowing and spending, which can help curb inflation by lowering aggregate demand.

- Lower Interest Rates: Encourage borrowing and spending, stimulating economic growth.

3. Economic Indicators

These are statistics that provide insights into the health and performance of an economy.

- Gross Domestic Product (GDP): Measures the total value of all goods and services produced within a country's borders in a specific period.

- Inflation: The general increase in the price level of goods and services over time.

- Unemployment: The percentage of the labor force that is willing and able to work but cannot find a job.

- Balance of Payments: A record of all economic transactions between residents of a country and the rest of the world.

4. Gross Domestic Product (GDP)

GDP is a key measure of economic output.

- GDP Formula: C + I + G + (X - M)

- C: Consumption (household spending)

- I: Investment (business spending)

- G: Government Spending

- X - M: Net Exports (Exports minus Imports)

- Real GDP: GDP adjusted for inflation, providing a more accurate measure of output changes.

- GDP per Capita: GDP divided by the population, indicating average output per person.

- Recession: Defined as two consecutive quarters of negative GDP growth.

- ⚠️ Limitation: GDP does not measure income inequality, environmental quality, or overall societal well-being.

5. Inflation

Inflation erodes purchasing power.

- Demand-Pull Inflation: Occurs when aggregate demand in an economy outpaces aggregate supply, pulling prices up.

- Cost-Push Inflation: Occurs when the costs of production (e.g., wages, raw materials) increase, leading firms to raise prices.

- Consumer Price Index (CPI): A common measure of inflation, tracking the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.

- 📊 Target: Many central banks aim for an inflation target of around 2%.

6. Unemployment

Different types of unemployment exist:

- Cyclical Unemployment: Caused by downturns in the business cycle (recessions).

- Structural Unemployment: Arises from a mismatch between the skills workers possess and the skills demanded by available jobs, often due to technological changes or shifts in industry structure.

- Frictional Unemployment: Short-term unemployment that occurs as workers move between jobs or search for new ones.

- Seasonal Unemployment: Occurs due to seasonal variations in demand for labor (e.g., agricultural workers, holiday retail staff).

7. Business Cycle

The economy experiences natural fluctuations over time.

- Boom: A period of rapid economic growth, high employment, and rising prices.

- Recession: A significant decline in economic activity spread across the economy, lasting more than a few months, normally visible in real GDP, real income, employment, industrial production, and wholesale-retail sales. (Often defined as two consecutive quarters of negative GDP growth).

- Trough: The lowest point of a recession, after which recovery begins.

- Recovery: A period of increasing economic activity, rising employment, and moderate growth.

8. Aggregate Demand (AD) and Aggregate Supply (AS)

These concepts describe the total demand and supply in an economy.

- Aggregate Demand (AD): The total demand for all goods and services in an economy at a given price level and time period (AD = C + I + G + (X - M)).

- Aggregate Supply (AS): The total supply of all goods and services produced in an economy at a given price level and time period.

- 💡 Impact: An increase in AD typically leads to both higher output and increased prices. An increase in AS, often due to improved productivity, can lead to economic growth with stable or falling prices.

📊 Business Analysis Frameworks

Beyond core economic theories, these frameworks help analyze the external and internal factors affecting businesses.

1. PESTLE Analysis

A strategic tool used to analyze the external macro-environmental factors that can impact an organization.

- Political: Government policies, political stability, trade regulations.

- Economic: Economic growth, inflation, interest rates, exchange rates.

- Example: High inflation reduces consumer spending power, impacting businesses.

- Social: Demographics, cultural trends, lifestyle changes.

- Technological: Innovation, automation, R&D activity.

- Legal: Laws, regulations, consumer protection.

- Environmental: Climate change, sustainability, resource availability.

2. Porter's Five Forces

A framework for analyzing the attractiveness and profitability of an industry.

- Threat of New Entrants: How easy or difficult it is for new competitors to enter the market.

- Bargaining Power of Buyers: The ability of customers to force prices down or demand higher quality.

- Bargaining Power of Suppliers: The ability of suppliers to raise prices or reduce the quality of goods and services.

- Threat of Substitute Products or Services: The likelihood of customers switching to alternative products or services.

- Rivalry Among Existing Competitors: The intensity of competition among firms already in the industry.

✅ Essential Formulas and Key Terms

Must-Know Formulas:

- GDP = C + I + G + (X - M) (Aggregate Demand/Output)

- PED = (% Change in Quantity Demanded) / (% Change in Price) (Price Elasticity of Demand)

- Profit = Total Revenue - Total Cost

- Average Cost (AC) = Total Cost (TC) / Quantity (Q)

Must-Know Keywords:

- Scarcity

- Opportunity Cost

- Elastic / Inelastic (Demand)

- Inflation

- Recession

- GDP (Gross Domestic Product)

- Monetary Policy

- Fiscal Policy

- Equilibrium

- Utility

💡 Conclusion: Interconnectedness of Economic Principles

The concepts outlined in this guide – from the microeconomic decisions driven by scarcity and opportunity cost to the macroeconomic performance measured by GDP and inflation – are deeply interconnected. Understanding the interplay between supply and demand, the impact of government policies, and the strategic insights offered by business frameworks like PESTLE and Porter's Five Forces provides a comprehensive lens for interpreting economic phenomena at various scales. Mastery of these principles is essential for informed decision-making in both academic and professional contexts.